Yes, in some instances a payday lender will have the right to take away your property previously pledged as collateral for the loan if you do not pay it back in full or on time.

It is important to note that this only occurs with secured payday loans, which refers to when a specific item of your property, known as collateral, guarantees payment of the debt. If you do not pay back the debts owed, and essentially ‘default’, then the payday loan lender has the right to take away your collateral, in the form of your home. This can only occur if the payday loan lender has a court order to enter your home – they need approval from a judge or a court clerk.

What Does it Mean if I Default on a Payday Loan?

Typically, if you miss one payment, you have defaulted on your payday loan. Under the majority of loan agreements, the lender is thus entitled to take the goods.

Furthermore, even if you make timely payments, but fail to comply with other important terms of your agreement, then the lender can also declare you to have defaulted and will thus take your property.

In some instances, you may even be considered to have defaulted on a payday loan even if you have paid completely if you sell the collateral, it is destroyed or the value of it substantially depreciates.

What Happens if I Default on a Payday Loan?

There are a number of steps that may follow if you have defaulted on a payday loan, for instance, if you have not paid in full or on time.

The first step is dependent on which US state you reside in. This is because a payday loan lender only has to notify you in advance that they are going to take away your property if you have defaulted if the specific state instructs them to do so. Typically however, unless the contract specifies otherwise, the payday lender must notify you that your full amount is due so that you have ample amounts of time to plan a repayment plan.

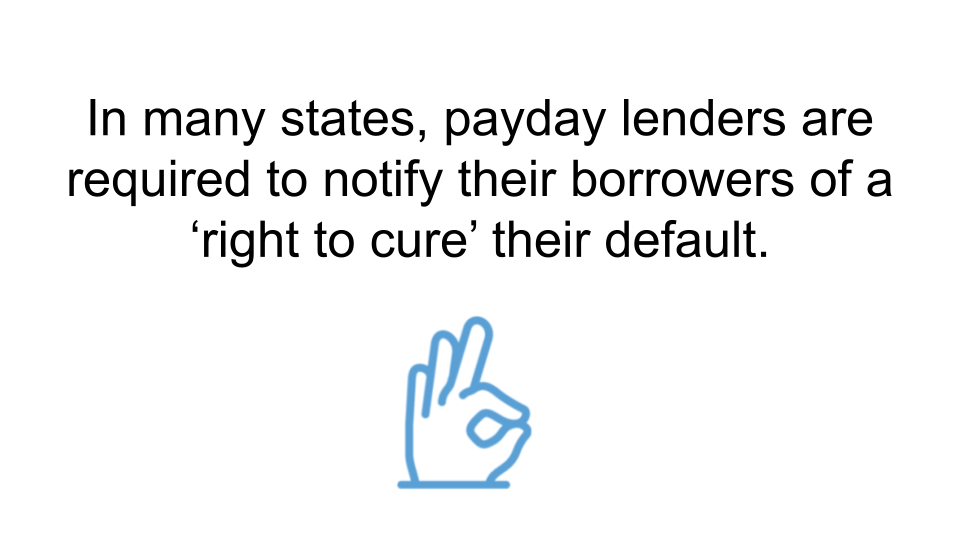

In many states, payday lenders are required to notify their borrowers of a ‘right to cure’ their default. This means that the borrower would get a certain period of time, typically a few weeks, to repay all of the missed payments as well as any late charges so that the defaulted situation is rectified.

If I Default, Does This Mean That I Will Automatically Lose my Home?

Payday lenders are unlikely to go ahead and take your home unless you have previously defaulted multiple times in the past, have missed several payments or are extremely uncooperative. As such, there are usually ways out of having your home taken away, especially if you have a previously positive track record when it comes to loans and repayments.

How can I get Out of a Situation Where I Have Defaulted on a Loan?

There are a number of ways that you can try to follow to get out of a situation that may lead towards your payday lender taking away your home. These include:

- Reaching out to your payday loan lender

If you anticipate that you will not be able to keep up with your payday loan repayments, then you should try to contact your payday loan lender as soon as possible. It is important that you fully explain your situation and make efforts to negotiate a payment plan with them to try and get back on track with the repayments.

The majority of payday loan lenders would much rather prefer to work with their borrowers to find a solution so that they do not reach a default stage, which would then involve the expenses and the hassle of collections for them.

- Seeking help

It is important to seek help if you are overwhelmed by your payday loan repayments. This help could come from a credit counseling agency, or even if your family and friends. Professional finance counselors can help by advising you on your options, as well as helping you to priorise your repayments and negotiate a new repayment plan with your payday loan lender so that you do not reach a default stage and have your property taken away.

A number of credit counseling agencies may charge a small fee for their services, but this may be waived in instances of financial hardship.

Further help could come from family or friends, who may be able to step in as guarantors for your payday loan. This means that if you are not able to repay your payday loan, they will step in and do it for you, instead of using your collateral such as your property to pay it off.

Are There Any Alternatives to Collateral Payday Loans?

Yes, there are alternatives to collateral payday loans, especially if you have a good credit score. Factors such as your affordability, income as well as credit score can be sufficient for approval from banks, credit unions and prospective payday loan lenders who do not require any collateral, such as your property.

An exception to the above however applies in the event of a mortgage application. Here, you may utilise your strong credit score to get the best rates possible while still having the mortgage loan secured against your property.

Further, in instances where you have a poor credit score and in need of borrowing money, it is important to remember that there are other alternatives available that do not require collateral. These may include charging higher rates of interest or fees, or lowering the amount of money that you are actually able to borrow. Further alternatives could also include adding on a guarantor with a good credit score to give both yourself and the payday loan lender additional security if you are no longer able to meet your repayments.