Loan applications may be rejected for a number of reasons, including failing to meet the basic requirements, having a poor credit score or outstanding loans or even when the lender does not have any additional capacity to lend more funds that month.

This article will list the reasons as to why your loan application may have been rejected, and the other possible routes that you may wish to go down to seek out funds.

What are the Reasons Why My Loan Application May Have Been Declined?

- Failing to Meet the Basic Criteria

Every US loan lender will have a minimum criteria that their prospective borrowers must meet in order to be eligible to apply for their loan. This could be for a personal loan, payday loan or title loan.

The minimum criteria that typically applies for most US lenders requires prospective borrowers to be over 18 years old, a US resident, be working full-time or part-time, as well as meet a minimum income requirement. This minimum may vary from lender to lender. Further, you will typically be required to have a valid checking account, valid email address, mobile number and no recent cases of bankruptcy.

If you do not meet the above criteria, then it is likely that your loan application will be declined.

- No or a Low Credit Score

When applying for a loan, your lender may carry out a credit check on you to understand your credit history and how responsible you are with making routine payments on time and in full. These may refer to credit card payments, loans and utility bills.

Some lenders may require their prospective borrowers to meet a minimum credit score requirement. If you exceed this, it is likely that your loan application will be approved. If your credit score falls below their set threshold, then it is likely that your loan application will be rejected.

This may also apply to those who do not have a credit score history at all, as it is makes it difficult for the lender to understand their capability to make the repayments on time and in full.

- Low Income

Income serves as a significant feature for lenders when they are determining a prospective borrower’s eligibility for a loan, as it is likely to serve as the main way in which they are going to repay the loan.

While it can vary from lender to lender, some may require your minimum earnings to fall between $800 to $1,000 a month. This is because they will consider the other financial commitments that you must meet, including rent, transport and food.

If your income is too low, the lender may suggest borrowing a smaller amount or will reject your application altogether if they do not believe that you will have the financial means to repay in full and on time.

- Poor Debt-to-loan Ratio

Lenders will additionally look at a prospective borrower’s debt-to-loan ratio, which fundamentally considers how much you are able to borrow vs. how much you are able to actually repay.

For instance, while your monthly income may cover the loan repayments, this may not consider the additional outstanding financial obligations that will need to be met, such as paying rent.

In some instances, a lender may evaluate your in-goings and outgoings and decide that you are not going to be able to repay the loan in full or on time, and thus reject your loan application.

In this case, it is worth negotiating with the lender to see if they will lend a smaller amount, or lengthen the loan repayment period to make the monthly repayment amounts ambler and easier to meet.

- Trust Factor

It is important to ensure that no mistakes are made on your loan application. This can impact the trust between a prospective borrower and their potential loan lender. For instance, make sure that your address history is accurate, as well as your monthly income amount.

If these are not accurate, the lender may pick up on this and decide to decline your loan application as they may not trust you to repay the funds in full and on time.

- Lack of Lender Capacity

In some instances, a loan lender may be unable to grant any further loans that month. This is because they do not have unlimited funds to hand out, and may only have a certain amount of loans that they can distribute each month.

As such, their criteria may be stricter depending on the month, and will only approve the top prospective borrowers. This may mean that if you do not meet their criteria fully then your loan application may be rejected.

Are Some US States Stricter with Loan Approvals than Others?

Yes, some US states are certainly stricter than others with their loan approval process. For instance, some states such as Nevada and Texas do not currently have any laws on how many outstanding loans an individual can have. While, in some states such as Ohio and Illinois, loan lenders will decline loan applications immediately if there is already one singular payday loan that is outstanding.

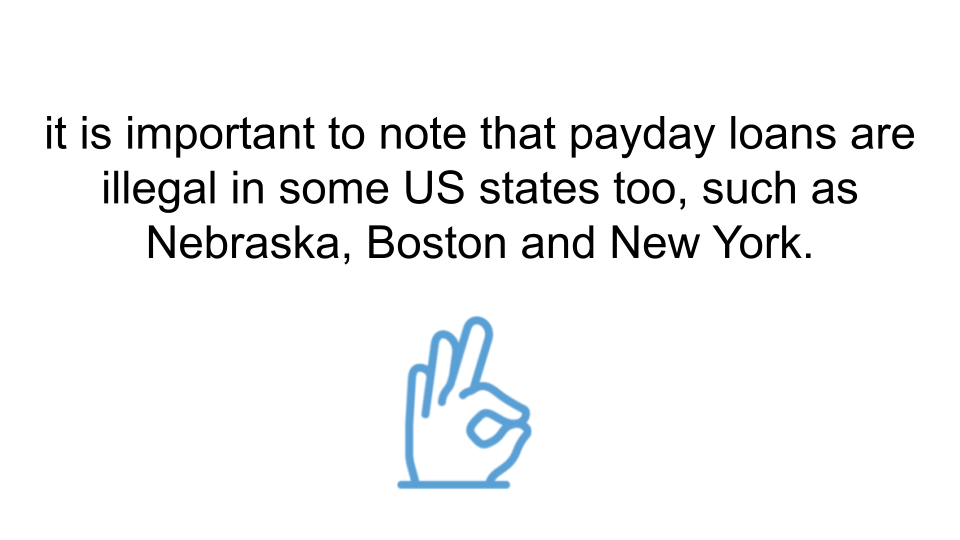

Furthermore, it is important to note that payday loans are illegal in some US states too, such as Nebraska, Boston and New York.

How Can I Increase My Chances of Loan Application Approval?

It is worth considering different ways that you can improve your credit score so that future loan applications are approved. Furthermore, if your loan application has been declined, you may ask the lender for feedback as to why this may have been the case. While lenders are not obligated to provide a response, they may wish to tell you so that they can secure potential lending business with you in the future.

Do not continue to apply for loans if your applications are recurrently declined, and ensure that you are taking the time to fill out applications accurately.